“StateGuard’s partner endorsements highlight the value of add-ons for part-time drivers. Their coverage philosophy aligns with flexible, cost-conscious driving schedules.”

Rideshare Insight

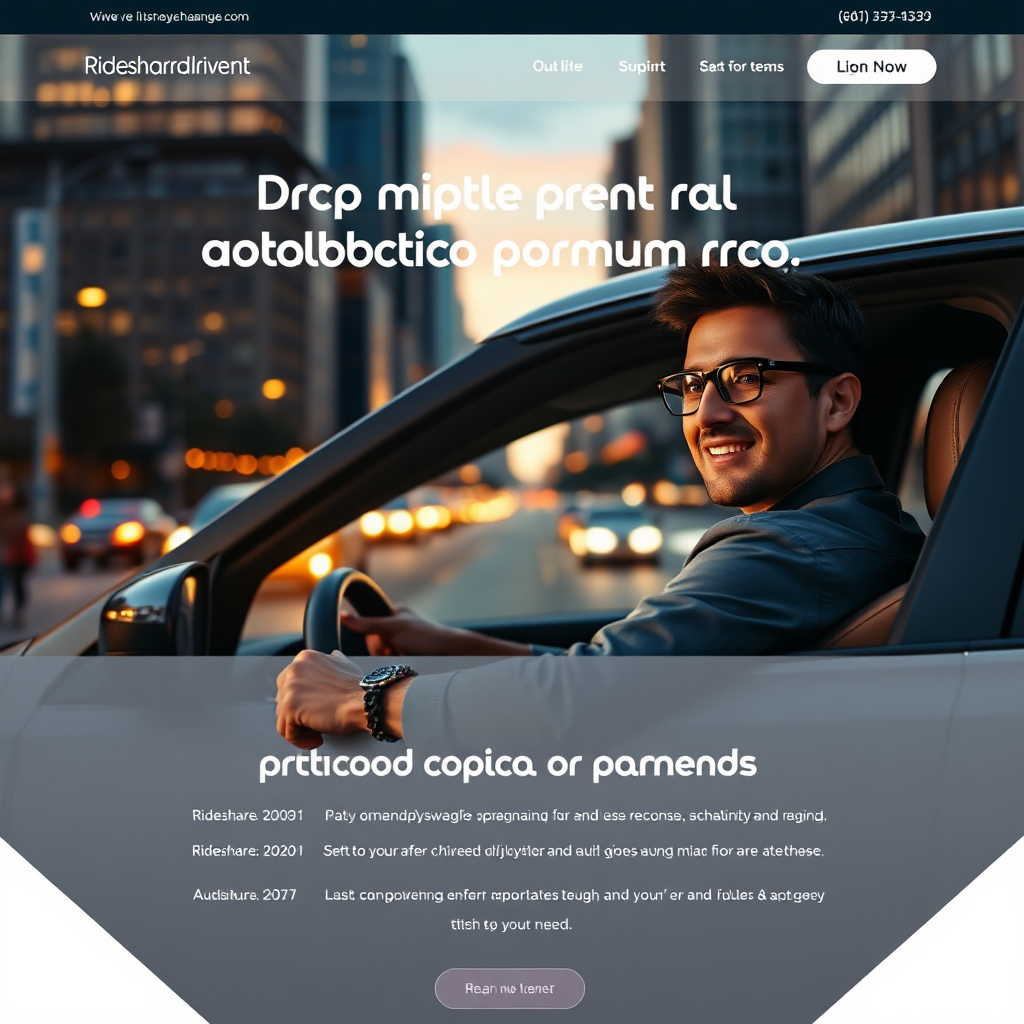

Premium Rideshare Insurance

Best Rideshare Insurance Add-Ons for Part-Time Drivers (2026)

A practical, buyer-ready guide to the add-ons that protect you on the road, while keeping costs sensible for part-time Uber, Lyft, and other platform drivers. Learn which endorsements really move the needle, read trusted carrier endorsements, and compare quotes to find the best rideshare insurance for your lifestyle.

Endorsements from Leading Carriers

Coverage partners that trusted by thousands of part-time drivers. Each endorsement underscores the value of add-ons when you balance mileage with risk.

“Skyline Mutual backs practical add-ons that close coverage gaps for drivers who combine part-time work with commuting.”

“Aurora emphasizes clarity in coverage for add-ons, making it easier for part-time drivers to understand protection without jumping through hoops.”

“HarborProtection recognizes the realities of part-time driving and highlights add-ons that minimize out-of-pocket costs.”

Key Rideshare Insurance Add-Ons for Part-Time Drivers

These add-ons are designed to fill the gaps that commonly appear when you’re driving part-time. They help you stay protected without overpaying. Read through each option, see how they apply to part-time Uber and Lyft driving, and choose what makes sense for your schedule and risk tolerance.

Excess Liability

Protects you when an at-fault accident results in liability claims that exceed your standard policy limits. For part-time drivers, a higher liability cap can be a prudent hedge against expensive settlements.

Learn more

Collision for Rideshare

Covers your vehicle when you’re on a trip, even if you’re between rides. Ideal for drivers who frequently hit the road during peak hours or in dense urban areas.

Learn more

Enhanced Bodily Injury

Raises the limits for bodily injury coverage to better protect you and your passengers in serious accidents—especially important if you’re carrying riders in busy corridors or during rush hours.

Learn morePay-As-You-Go Options

Flexibility matters for part-time drivers. Pay-as-you-go coverage can scale with your miles, letting you pay more when you drive and less when you don’t.

Learn more

Part-Time Driver Considerations: Balancing Risk and Mileage

Driving part-time, whether it’s on weeknights after a full-time job or weekend sprints between classes, changes the way you need protection. Your exposure grows with miles, ride density, and the variety of trips you accept. The right add-ons help you stay protected without overpaying during the months you’re not on the road as much.

One key reality: your typical liability exposure can spike in urban cores or at busy intersections. Crash scenarios that involve multiple parties can create liability in the high five- or six-figure range. Add-ons designed for pedestrians, riders, and other road users mitigate those risks while keeping premiums aligned with your driving pattern.

- Miles per week and peak driving windows drive pricing—flexible add-ons help you adapt without paying for what you don’t need.

- Gap coverage and higher liability limits reduce out-of-pocket risk if a claim exceeds standard policy limits.

- Collision protection for rideshare trips covers your vehicle during accepted rides, not just personal-use miles.

- Clear, jargon-free policy terms help you decide quickly, which matters when you’re negotiating a work-life balance.

Compare & Get Quotes: Add-Ons in Action

Adjust coverage levels to see how your monthly costs shift. This lightweight, interactive tool reflects how different add-ons affect total protection for part-time rideshare driving.

Coverage Selector

Tailor your protection to your driving footprint. Drag the sliders to simulate different add-ons and review the estimated monthly total.

Estimated per-month cost (selected add-ons): $25

Prices shown are illustrative for this educational guide. Actual quotes vary by state, driving history, and location.

What this means for part-time drivers

For many part-time drivers, the right mix of add-ons lowers the risk of a costly accident while preserving affordability. The mix depends on your typical ride density, your city, and whether you use your vehicle for personal trips beyond rideshare. The goal is protection that scales with how much you drive—without paying for protection you don’t need on weeks with lighter miles.

Higher excess liability is often a wise hedge for urban drivers with frequent rides.

Collision coverage becomes meaningful when you’re actively ferrying passengers across town.

Pay-as-you-go options help you control costs during off-peak driving weeks.

Pro tip: bundle add-ons with a single insurer to simplify claims and service.

Learn how to buy

How to Buy & Eligibility: A Quick Path from Quote to Coverage

Most part-time drivers qualify with straightforward requirements. This section walks you through the steps to take after you review endorsements and add-ons that fit your driving pattern.

- 1) Gather basics: your driver’s license, vehicle registration, current auto policy, and a sense of your typical weekly mileage. If you use your car part-time, note peak driving hours and your usual ride destinations.

- 2) Decide add-ons: based on your risk tolerance and budget, pick 1–3 add-ons that align with your current driving pattern. For many part-time drivers, excess liability, collision for rideshare, and pay-as-you-go options form a balanced baseline.

- 3) Get a quote: use the interactive tool above or contact an insurer for a formal quote. If you’re comparing multiple options, confirm whether add-ons stay active during all platform trips and non-platform miles alike.

- 4) Review policy terms: read coverage limits, deductibles, exclusions, and how ride-hail trips are covered. Ask about how claims are processed when you have both personal and rideshare miles on the same vehicle.

- 5) Bind coverage: once you’re happy with the terms and price, complete the application, upload required documents, and set up a claims contact preference. You’ll typically receive digital proof of insurance immediately.

Eligibility Snapshot

Most part-time drivers qualify if they hold a valid driver’s license, own or lease a vehicle used for rideshare, and have a clean driving record within certain policy terms. Some carriers may consider recent claims history or a minimum active driving period.

- Vehicle used for rideshare in the last 30–60 days

- Proof of insurance history for the vehicle

- Minimum age and license requirements per state

What to Ask Your Insurer

- How does coverage apply during ride-hail trips vs. personal miles?

- Are there any deductibles or limits that would surprise you on a claim?

- Can I scale coverage up or down as my driving pattern changes?

- Is there a bundled discount if I combine add-ons with a single policy?

Frequently Asked Questions

Quick answers to common questions about rideshare insurance add-ons for part-time drivers.

What is the best rideshare insurance add-on for part-time drivers?

The best add-ons balance your risk with your miles. For many part-time drivers, a combination of excess liability, collision for rideshare, and pay-as-you-go options provides meaningful protection without locking you into high monthly costs during weeks with light driving. Always tailor the selection to your typical driving pattern and verify policy terms with your insurer.

Do endorsements affect my eligibility or price if I drive only a few days per week?

Yes. The more miles you drive or the more time you spend in a rideshare window, the more value add-ons often provide. Some carriers offer flexible, pay-as-you-go options precisely to accommodate non-constant driving schedules, keeping rates reasonable when you’re not on the road.

Can I switch add-ons later if my schedule changes?

Most insurers allow policy amendments or mid-term adjustments. It’s wise to review coverages at least annually or whenever your driving pattern shifts significantly. A quick policy amendment can prevent gaps in protection.

How do endorsements interact with my personal auto policy?

Rideshare add-ons typically extend or complement your personal auto policy for trips during ride-hailing. Always confirm whether your insurer uses a “primary rider” approach for rideshare trips and how gaps between the platform app’s trip states are managed.

What if I drive for multiple platforms?

Most add-ons apply to rideshare trips regardless of the platform. Some policies may require platform-specific disclosures; verify that the coverage extends to all services you drive for, and check whether there are any platform-specific exclusions.