Income Reporting for Freelancers

If you work for yourself, your Marketplace eligibility hinges on how your yearly income is reported. You’ll use self-employment forms (like Schedule C) to detail earnings, and you’ll estimate quarterly taxes to stay compliant. Accurate reporting helps you access subsidies when you qualify and ensures you avoid gaps in coverage.

The Marketplace uses your reported income to determine your expected annual premium and the amount of the Premium Tax Credit (PTC you may receive as a subsidy). When income fluctuates—typical for freelancers—your eligibility can shift from year to year, so it’s important to review your status during Open Enrollment or after a qualifying life event.

Subsidy Eligibility & Calculation

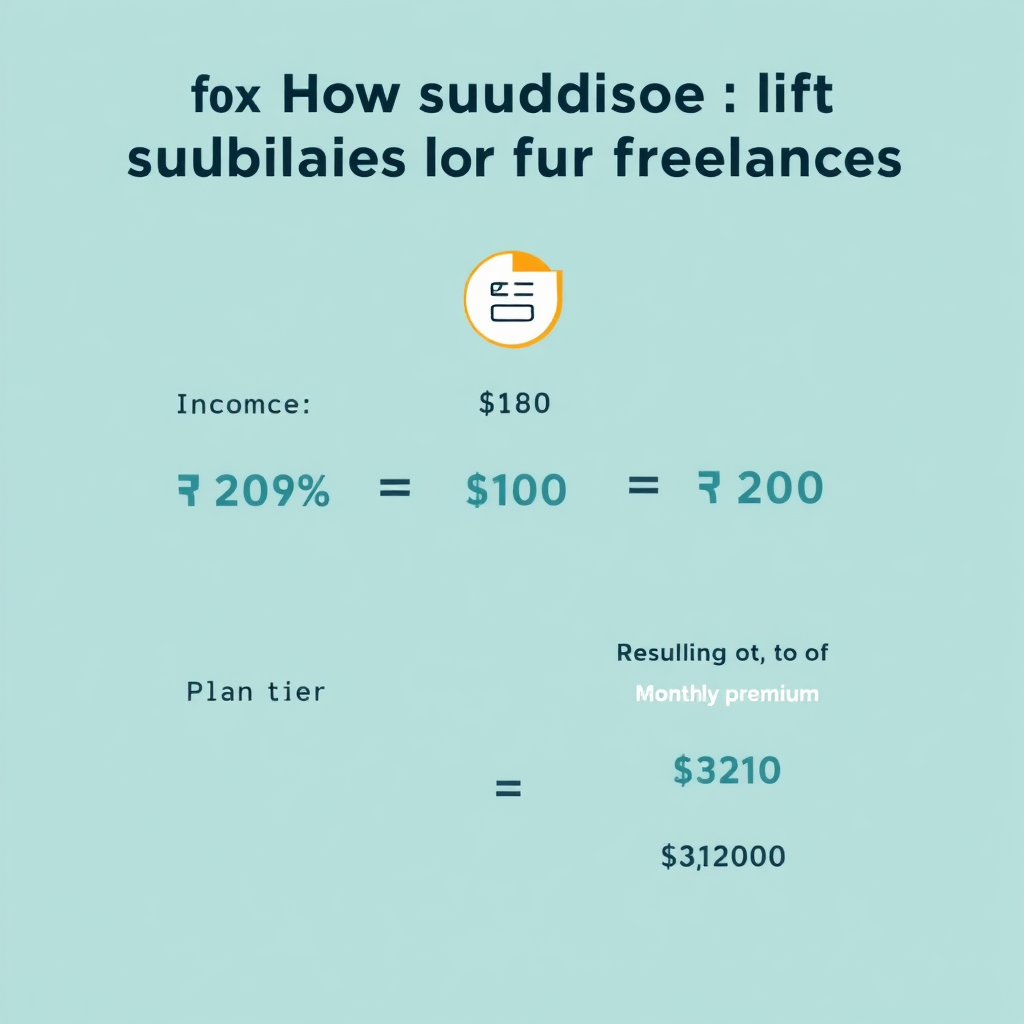

Most freelancers earning between about 100% and 400% of the Federal Poverty Level (FPL qualify for the Premium Tax Credit, which lowers monthly premiums. The exact amount depends on household size, total income, and plan choice. This section provides a practical, illustrated calculator to give you a sense of potential savings. Note that eligibility and subsidy amounts are determined by the Marketplace when you apply.

Illustrative calculation based on plan type and income as a share of the Federal Poverty Level (FPL). Official subsidies vary by year, household, and plan.

—

Illustrative subsidy calculator (interactive). Values are for demonstration only.

Special Enrollment Periods (SEPs)

SEPs let you enroll in a Marketplace plan outside the Open Enrollment period if you have qualifying life events. For freelancers and gig workers, common triggers include losing other health coverage, moving, getting married, or welcoming a new dependent. Knowing the deadlines helps you avoid gaps in coverage.

- Loss of coverage: You or a household member loses qualifying health coverage.

- Gaining a dependent through birth, adoption, or foster care.

- Marital status change or moving to a new ZIP code.

- Other qualifying life events recognized by the Marketplace.

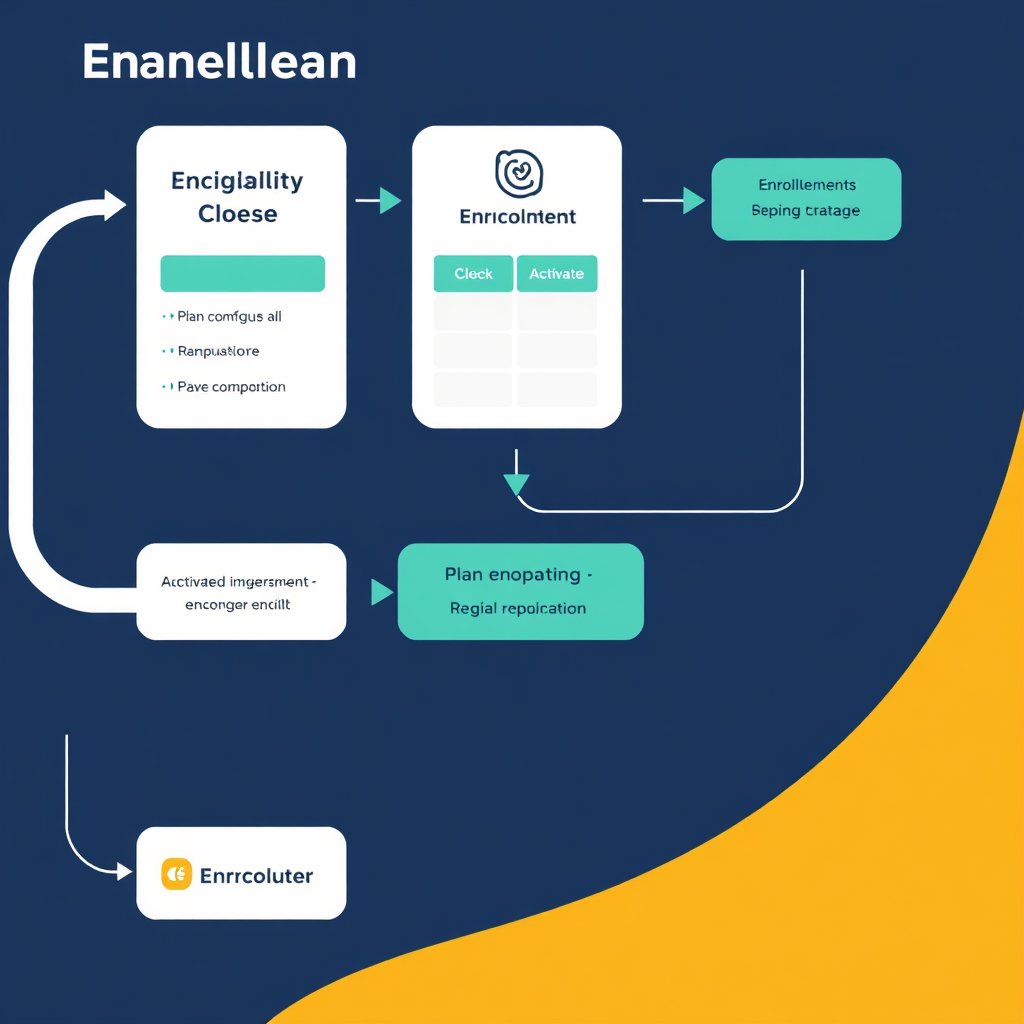

Enrollment Process Overview

Set up a marketplace account to access personalized plan options and subsidy estimates.

Enter income, household size, and any dependents to determine plan options and subsidies.

Review Bronze, Silver, and Gold across premiums, deductibles, and networks.

Submit your selection, confirm eligibility, and activate coverage with the plan start date you choose.

Keep copies of income docs and plan details for your records and future SEP considerations.

Opt in for renewals so changes in income won’t catch you by surprise in the next year.

Documentation & Tips for Freelancers

Staying organized makes Marketplace enrollment smoother. Below are common questions and practical tips to help freelancers navigate income reporting, subsidies, and enrollment timelines.

Do freelancers qualify for subsidies?

Subsidies (Premium Tax Credits) are available to households within 100–400% of the Federal Poverty Level. Eligibility depends on income, household size, and chosen plan. If your income fluctuates, you may qualify in some years but not others—so monitor your status during Open Enrollment.

What documents should I prepare?

Typical documentation includes proof of income (recent tax return or pay stubs), proof of identification, and information about household members. If you’re self-employed, keep up-to-date records of business income and expenses to support any subsidy calculations.

When is the best time to enroll?

Open Enrollment runs yearly for most plans. If you experience a qualifying life event—such as a change in income, a move, or gaining a dependent—you may qualify for a Special Enrollment Period to enroll outside the standard window.

How does income affect subsidies?

Your reported annual income and household size determine your position on the Federal Poverty Level scale. Higher-income households may receive smaller subsidies, while lower-income households in the eligible range can receive larger subsidies. The marketplace recalculates subsidies each year based on your updated information.

Ready to explore coverage options?

Use the subsidy estimator to gauge potential savings, review plan types, and prepare government-required income documentation for a smooth enrollment experience. This section keeps you focused on next steps without ambiguity.